Credit Portfolio Risk Analysis

Deep Analytical Insights and Evidence-based Forecasting

Application of Complex Mathematics to Financial Products

Euler Consulting is a specialist advisory firm specialising in credit portfolio risk analysis. .

- Portfolio performance, loss analysis, forward forecasting. Asset classes include corporate loans, vehicle and personal loans

- Economic Capital modelling and integration into management decision making and business operations

- SRT (Significant Risk Transfer) synthetic portfolio transaction structuring and execution

Proposal to Amend Regulation (EU) 2017/2402

In June 2025 the European Commission published its proposed amendments to regulation 2017/2402.

Review and commentary on the proposals

Law firm Mayer Brown published its review of the proposed amendments in July 2025. They conclude:

Overall, however, the proposals, if implemented in close to their current form, should be a major boost to the EU securitisation market.

Credit Portfolio Insights – South Africa

I’ll be sharing regular views on credit portfolio management in South Africa—focusing on commercial and economic impact rather than regulatory or accounting detail.

On 1 July 2025, the South African Reserve Bank introduced new capital rules, phasing out Internal Ratings Based (IRB) models in favour of the Standardised Approach (STA).

Basel Committee

on Banking Supervision – Synthetic Risk Transfers

This is a recent (and rare) comment from BCBS on synthetic securitisation. Overall it is a positive statement about the genre.

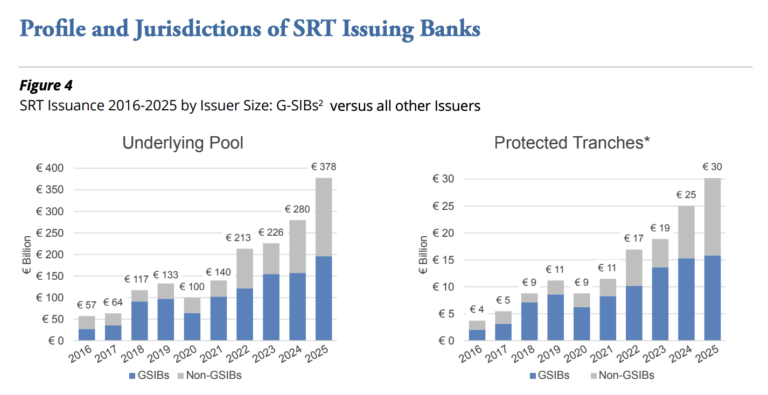

IACPM Global SRT Bank Survey 2016-2025 Results Released

The IACPM released the results of its annual Global SRT Bank Survey on risk sharing transactions executed by banks through synthetic on balance-sheet securitizations. Read More…

About Euler Consulting

Our Founder, Greg Wakelin, has over 30 years experience spanning credit portfolio management implementation and modelling, structured credit trading, traded risk management and SRT structuring.

He has worked in New Zealand, Australia, London, South Africa in analytical and front office roles.

His passion is to bring the science of portfolio analysis to life in real transactions.

Greg Wakelin - Full Biography

Greg Wakelin has worked in the area of credit portfolio analytics almost all his working life.

Greg began his career as an actuarial clerk for NZI Life in Auckland New Zealand. In the mid 1990s, at ANZ Bank in Melbourne, Australia, he worked on the first Economic Value Add project.

Firstly he looked at interest rate risk modelling and basis risk, but then started on the implementation journey of the first KMV Corporation Portfolio Manager software. The fundamentals in this software are still used today in commercially available packages. From the software he build the data flows, the analysis, and then moved into business role to assist origination in the context of the portfolio model. The next step within ANZ was to set up their very first Credit Portfolio Management function.

Still at ANZ, Greg became an expert in the growing Credit Derivative product. In 2001, he moved from the CPM function onto the bank’s credit trading desk. The desk established and executed the first credit linked and structured notes, and shortly after Greg become head of credit trading.

With the significant growth in the local and global credit derivative market, the credit trading business was split into a Structured Credit team, and (traditional) credit trading team. Greg became Head of Structured Credit. This team grow and the business flourished until mid 2007 when the US market took and bad turn that lead to the GFC in 2008.

In early 2008 Greg was appointed to Head of Global Markets, UK and US for ANZ Bank, and relocated to London from Sydney.

Until end 2010, Greg ran a ~70 person business through the depths of the Global Financial Crisis. This was a truly momentous time for global markets, where the London trading floor became a critical access point to liquidity for the Australian bank through the GFC.

At the end of 2010 Greg returned to Sydney. At somewhat of a cross road career wise he took some time out, and re-emerged in South Africa!

Greg worked as the Head of Finance for an NGO for a period before consulting to Libfin in 2015/2016. There the focus was on Economic Capital embedment into frontline origination, and also deep dive on valuations of the structured notes, and writing a technical report on the portfolio performance with a view to opening the activity up to third party funding.

In 2017 Greg started at Absa Bank (then Barclays Capital). This is where he still works as a consultant. The role there has been fundamentally Global Markets based, but with touch points into client portfolio risk analysis (private banking book credit through public securitisation) and economic capital front office embedment.

He is currently the lead on developing Absa’s (and South Africa’s) first Significant Risk Transfer transaction.

In all of Greg’s roles he has brought value in being able to straddle technical and detailed credit portfolio dynamics and commercial implementation.

He is not a quant per se, he is not an originator per se, but plays a critical role in communicating with clients and origination and credit risk teams on the risk and return profiles.

Dev:

Source: https://www.reddit.com/r/mathematics/comments/17q51a5/exploring_the_beauty_of_eulers_formula_in_3d/